KOHO is a Canadian online bank with competitive interest rates and an attractive cashback program offering up to 5% cash back on your purchases. There are no monthly fees for KOHO’s basic account, and with a KOHO Premium account, you pay zero fees on foreign exchange.

However, many Canadians complain about not receiving their KOHO referral bonus, and signing up for a bank account without a bonus is a bummer. Instead, I recommend signing up for TopCashback, a cashback portal offering a $15 signup bonus plus discounts of 10% or more on thousands of brands.

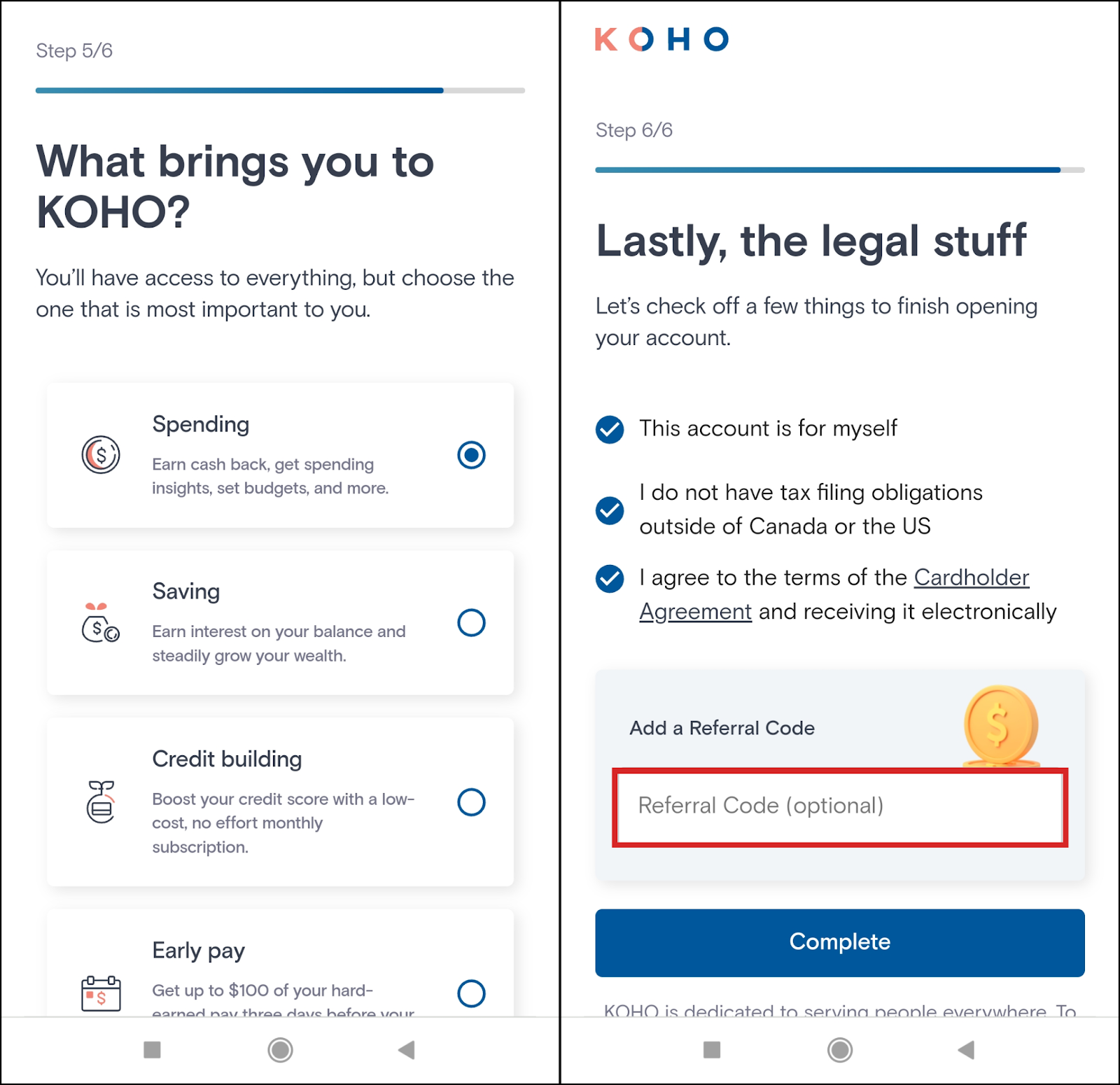

How To Use A KOHO Referral Code

KOHO has a referral program in place for new clients. By using our referral link (no code required), you’ll receive a $20 signup bonus—the highest in Canada—plus these additional benefits:

- $20 signup bonus

- 0.50% cash back on all purchases

- Up to 5% cash back at select retailers

- 1.20% interest on your balance

To use the promo code:

- Visit KOHO’s website and click Open An Account.

- Fill in your basic information, such as name, email, and mobile number.

- After you fill out your address, occupation and what brings you to KOHO, you will be prompted to Add a Referral Code. No code is required since you used our link, so you can skip this step.

Once you have a working KOHO account, you can request your KOHO prepaid Mastercard. It’s a great choice for people with bad credit.

What Is KOHO?

KOHO is one of the most popular online banks in Canada and was launched back in 2017. It bases its user experience on having the highest-rated mobile app, which grants a lot of customization and power to the user and their spending. It’s also well known for its ample cashback rewards and the broad usability it carries within.

KOHO is also a federally chartered bank in Canada and a Canada Deposit Insurance Corporation (CDIC) member. It is a completely digital bank with no physical location that provides great credit card options for Canadians and is available in all provinces. Here’s our full KOHO review.

KOHO Features

- 0.50% cash back on all purchases (up to 5% at select stores).

- 1.20% interest on all your balance.

- Early Payroll (up to 3 days early)

- Unlimited free Interac e-Transfers and online transactions.

- No monthly fees.

- Joint savings accounts.

KOHO Fees

KOHO can be used abroad without any trouble at all. Its fees might seem large but they’re comparable to the fees offered by other online banks.

Free Account:

- No minimum balance.

- Monthly fee: $0.

- Foreign ATM fees: 1.5% + $3.

- Foreign spending fees: 1.5%.

- Foreign exchange fees: 1.5%.

Premium Account:

- No minimum balance.

- Monthly fee: $9 (or $84 per year).

- Foreign ATM fees: 1.5% + $3 (1 free withdrawal per month).

- Foreign spending fees: 1.5%.

- Foreign exchange fees: Free.

How To Sign Up For KOHO

#1 Visit KOHO’s website and click Open Account.

#2 Fill in some basic information, like your name, phone number, and address. Keep in mind that to receive your card you need a Canadian address.

#3 Choose your primary reason for using KOHO (spending, savings, credit building, etc.). This won’t limit your access to any service, this is just so KOHO can focus on areas to improve.

#4 Finally, you’ll be asked to enter your referral code. Since you used our link, you can skip this step.

KOHO’s Referral Program

After creating your KOHO account, you can find your referral code in the app, in the Perks tab.

- Share your code via text, email, or to your social media audience.

- Once a referee signs up and makes their first purchase within 30 days of registration, you and your referee will receive a $20 credit.

- You can refer a maximum of 50 friends for a total of $1,000

Is KOHO Safe & Legit?

The first thing to mention here is that all online banks we reviewed are completely safe, with KOHO having the most safety features. Since KOHO is partnered with Peoples Trust, it’s automatically regulated and insured by CDIC, with every eligible deposit being insured for up to $100,000 CAD.

On top of that, KOHO’s users can freeze/unfreeze their cards whenever they want and set up biometric login authentication for a safer sign-in process. However, users can’t reset their card PINs from the app.

Onto another topic in the same vein, KOHO has the benefit of performing a soft credit check whenever a user creates a bank account, which means that KOHO can be used without harming credit scores, and it even has a credit-building feature.

In Summary

Overall, KOHO is a good online bank with plenty of features, including zero monthly fees on its basic account and zero foreign exchange fees with a KOHO Premium account. However, many Canadians complain about not receiving their KOHO referral bonus, so we don’t recommend signing up with them if you’re seeking a bonus.

Instead, I recommend signing up for TopCashback, a cashback portal offering a $15 signup bonus plus discounts of 10% or more on 7,000+ brands. The average TopCashback user saves $450/year, so it’s a great time to open your account and start saving.