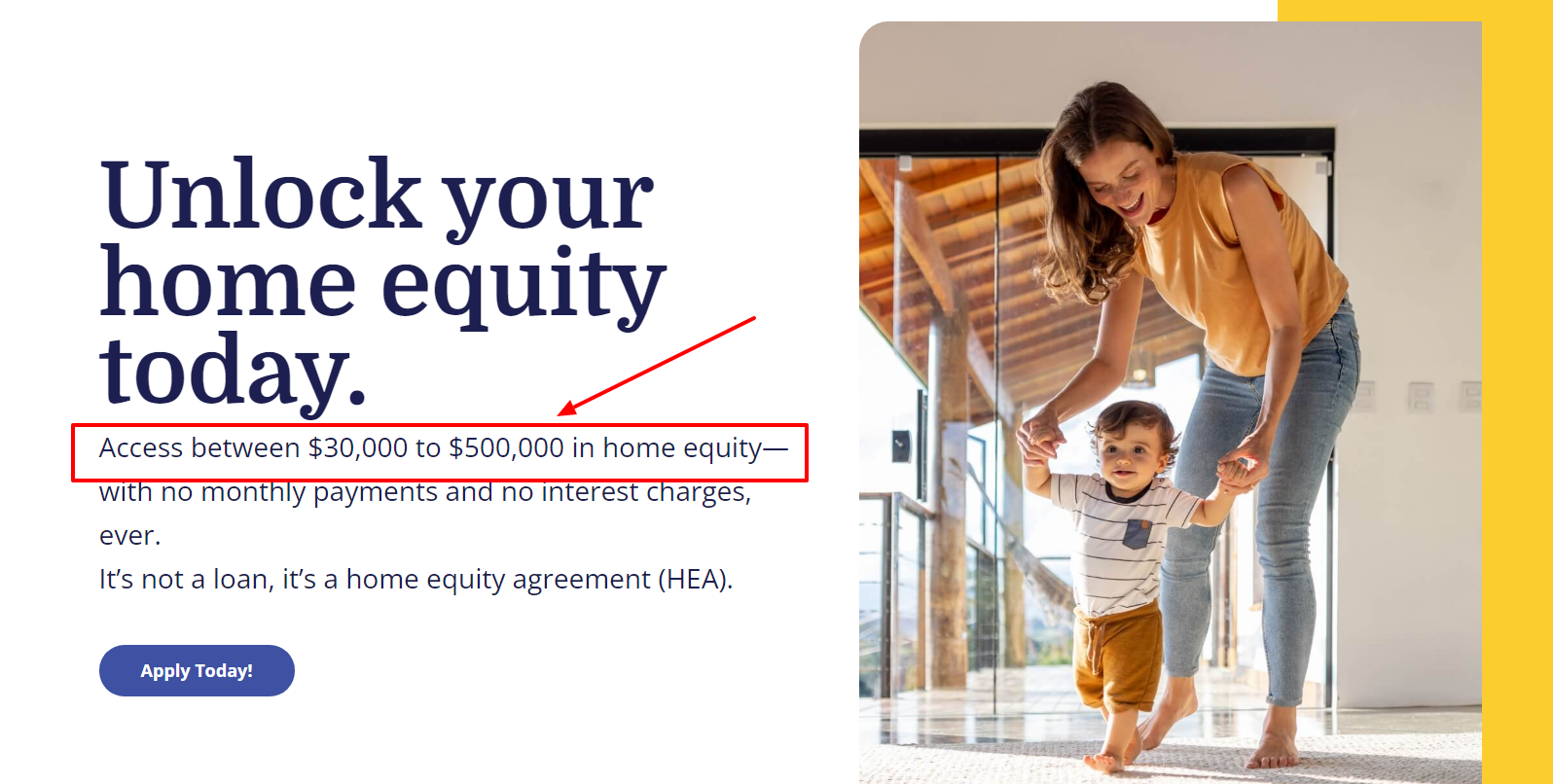

If you are looking for an alternative way to access your home equity without taking on debt, you might want to consider a home equity agreement (HEA) with Unlock. Unlock is a real estate investment company that offers HEAs to homeowners who want to trade a percentage of their home’s future value for cash today. In this Unlock review, you’ll learn that you don’t have to pay any interest or monthly payments on the cash you receive from Unlock. You only need to have at least 30% equity in your home and a FICO score of only 500 to qualify for a HEA.

Unlock is a great option for homeowners who want to access their home equity without adding financial stress or risk. It is especially suitable for homeowners who have bad credit, low income, or irregular income sources and who plan to sell their home or pay back the debt in the next 10 years.

Unlock is not a good option for homeowners who want to keep all of their home’s equity and appreciation potential and who do not want to pay an origination fee and other costs upfront. It may not be the best choice for those who have good credit and sufficient income to qualify for a traditional home equity product and prefer to pay interest and monthly payments on a fixed term and amount.

If you are interested in getting a HEA with Unlock, you can create an account on their website and see your preliminary terms in minutes.

If you are a homeowner, you might have a lot of equity in your home that you want to access for various purposes. However, you might not want to take on debt or pay interest or monthly payments on a home equity loan or a HELOC. Is there another way to tap into your home equity without taking on debt? Yes, there is. It’s called a HEA with Unlock. In this unlock review, we will explain what a HEA is, how it works, what are the pros and cons of getting one with Unlock, and how to get started with them. Read on to find out more.

What Is Unlock?

Unlock is a real estate investment company that offers home equity agreements (HEAs) to homeowners who want to access their home equity without taking on debt. HEAs are different from traditional home equity loans or HELOCs because they do not charge interest or require monthly payments. Instead, you agree to share a percentage of your home’s future value with Unlock when you sell your home or at the end of the term, which is typically 10 years.

Unlock was founded in 2019 by Jim Riccitelli and Dan Foster. They wanted to create a new way for homeowners to unlock their home equity without adding financial stress or risk. Unlock is based in New York, and operates in 15 states across the US.

Features Of Unlock

Unlock has some unique features that make it stand out from other home equity products. Here are some of them:

#1 No Credit Score Or Income Requirement

Unlike most lenders, Unlock does not base its approval on your credit score or income. You only need to have at least 30% equity in your home and a FICO score of only 500 to qualify for a HEA with Unlock. This means you can get approved even if you have bad credit, low income, or irregular income sources.

#2 No Interest Or Monthly Payments

One of the biggest advantages of a HEA with Unlock is that you don’t have to pay any interest or monthly payments on the cash you receive. You only pay back Unlock when you sell your home or at the end of the term, whichever comes first. The amount you pay back is based on a percentage of your home’s future value, which is agreed upon upfront. For example, if you receive 10% of your home’s value today from Unlock, you might pay back 18.5% of your home’s value in the future.

#3 Flexible Use of Funds

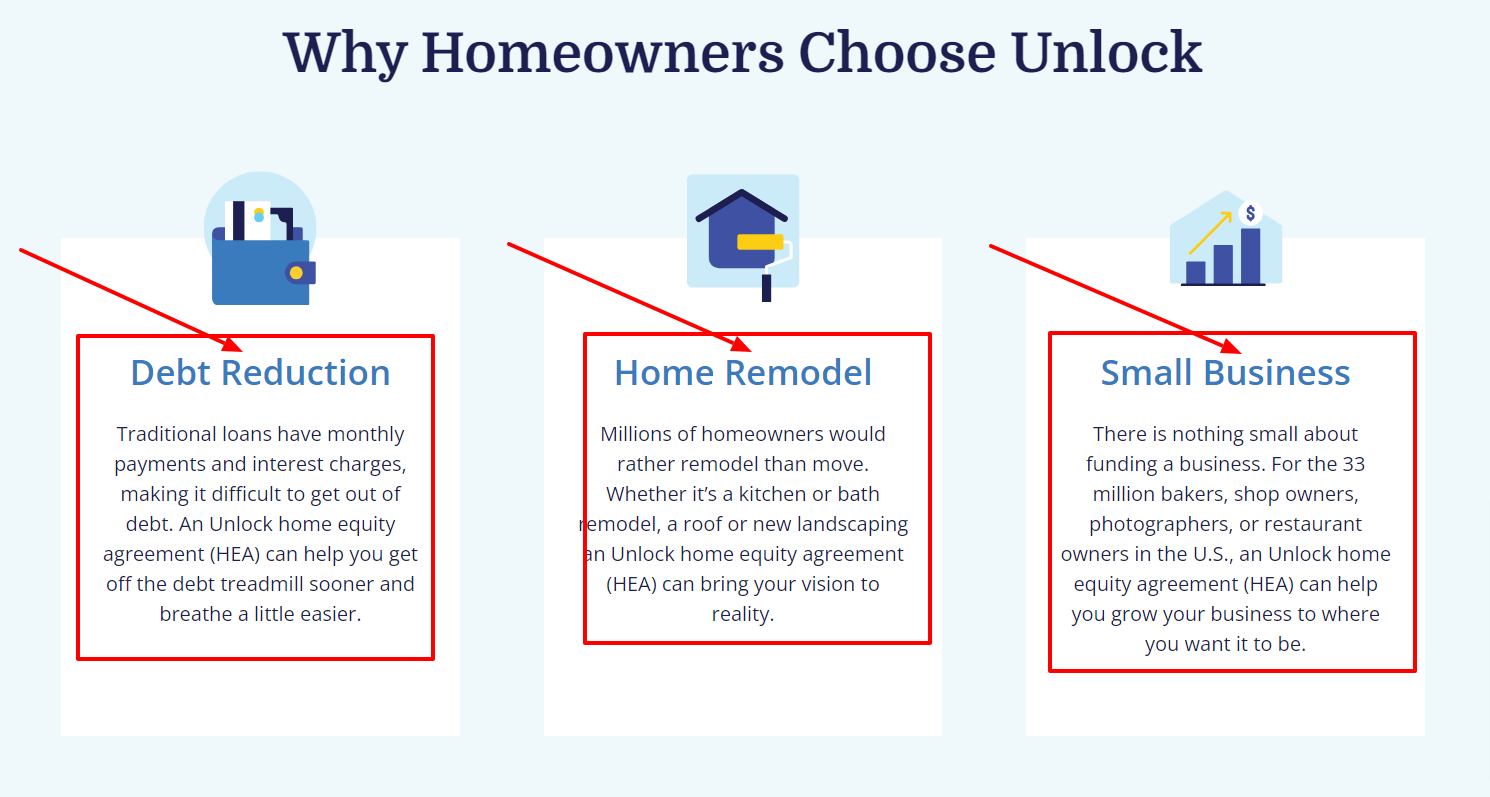

Another benefit of a HEA with Unlock is that you can use the cash for any purpose you want. Whether you need to pay off debt, fund a home improvement project, start a business, invest in education, or simply boost your savings, you have the freedom to use the money as you see fit.

#4 No Prepayment Penalty

If you decide to pay back Unlock before the end of the term, you can do so without any penalty or fee. You can also buy out your agreement at any time by paying back the original amount plus an annualized return that varies depending on how long you have had the agreement. For example, if you received $50,000 from Unlock and want to buy out your agreement after two years, you might pay back $57,500 ($50,000 + 7.5% annualized return).

#5 Shared Risk and Reward

With a HEA with Unlock, you share both the risk and reward of your home’s future value with Unlock. If your home appreciates in value over time, you will pay back more than what you received from Unlock. However, if your home depreciates in value over time, you will pay back less than what you received from Unlock. In fact, if your home loses more than 30% of its value at the time of sale or buyout, you will not owe anything to Unlock.

How To Get Started With Unlock

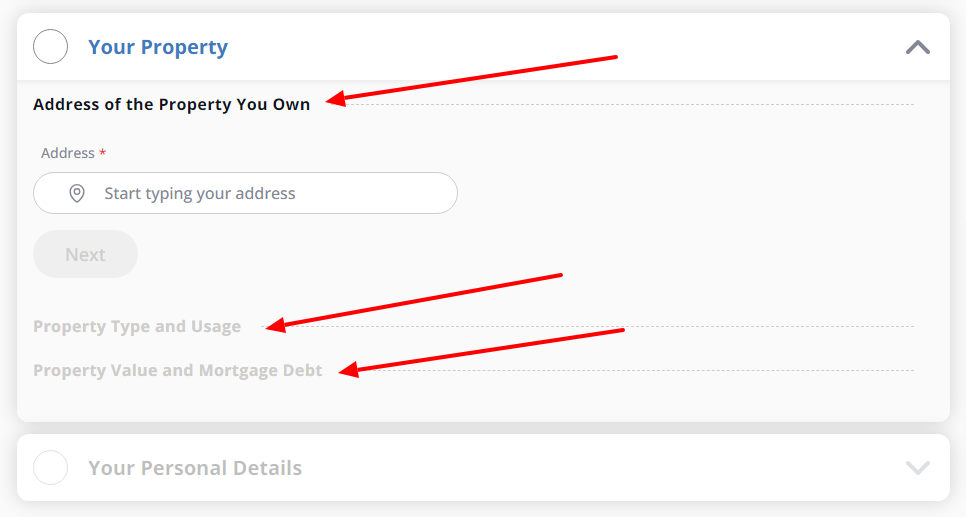

If you are interested in getting a HEA with Unlock, you can create an account on their website and see your preliminary terms in minutes. You will need to provide some basic information about yourself and your home, such as:

- Your name.

- The address of the property you own.

- Type of property.

- The property’s value and mortgage debt.

You will also need to upload some documents, such as your mortgage statement, proof of identity, and proof of homeowners insurance.

Once you submit your application, Unlock will review it and send you a final offer within a few days. If you accept the offer, you will need to schedule an appraisal and an inspection of your home, which Unlock will pay for. After that, you can sign the agreement and receive your cash in as little as 30 days or even less if the appraisal goes smoothly.

Pros Of Unlock

Here are some of the pros of getting a HEA with Unlock:

- You can access your home equity without taking on debt or paying interest or monthly payments.

- You can qualify for a HEA with Unlock even if you have bad credit, low income, or irregular income sources.

- You can use the cash minus certain required expenses, for any purpose you want, such as paying off debt, funding a home improvement project, starting a business, investing in education, or boosting your savings.

- You can pay back Unlock at any time when you sell your home without penalties or extra fees, or you can settle with Unlock after 10 years.

- You share both the risk and reward of your home’s future value with Unlock. If your home loses value over time, you will pay back less than what you received from Unlock.

Cons Of Unlock

Unlock is a great option for most homeowners, but it does have some caveats. Here are some of the cons of getting a HEA with Unlock:

- You will pay back more than what you received from Unlock if your home appreciates in value over time. This is based on the “shared risks and rewards” business model.

- You will give up some of the equity and appreciation potential of your home to Unlock.

- You will pay a 4.9% origination fee and other third-party costs upfront, which will reduce the amount of cash you receive from Unlock.

- You will need to have at least 30% equity in your home and a minimum FICO score of 500 to qualify for a HEA with Unlock, so it’s not an option for homeowners with a new mortgage.

- You will need to sell your home or buy out your agreement at the end of the term, which is typically 10 years.

Unlock Pricing

One of the most important factors to consider when getting a HEA with Unlock is the pricing. Although you don’t have to pay any interest or monthly payments on the cash you receive from Unlock, you do have to pay some upfront costs and a percentage of your home’s future value when you sell your home or at the end of the term.

The upfront costs include a 4.9% origination fee and other third-party costs, such as appraisal, inspection, title, escrow, and recording fees. These costs will reduce the amount of cash you receive from Unlock upon closing your agreement.

Let’s break these costs down with an example.

Example Breakdown Of Unlock’s Pricing

Suppose your home is worth $500,000, and you still owe $200,000 in your mortgage (your equity is $300,000). Under these conditions, you can qualify for up to a $110,000 HEA. Now let’s say you take a 10% HEA ($50,000) from Unlock. In this case you’ll pay an origination fee of $2,450 and around $1,500 in other third-party costs, which means you will receive around $46,050 in cash upon closing in exchange for 20% of your home’s value after 10 years. That’ll be $100,000 if the value doesn’t change, but if your home appreciates at, say 3% annually, it’ll be worth around $675,000 after 10 years, so you’ll have to pay Unlock approximately $135,000 once you sell.

Here’s a table summarizing the costs of this example.

| Current home value | $500,000 |

| Upfront Costs (4.9% origination fee + third-party costs) | $2,450 + approx. $1,500 = approx. $3,950 |

| You’ll receive (10% equity – upfront costs): | Approx. $46,050 |

| Hove value upon settlement* | $675,000 |

| You will pay back (upon settlement)* | $135,000 |

| Total cost | $88,950 |

The percentage of your home’s future value that you pay back to Unlock is agreed upon upfront and depends on several factors. These factors include your home’s current value, your equity percentage, your FICO score, and the local market conditions. For example, if you receive 10% of your home’s value today from Unlock, you might pay back 18.5%–22% of your home’s value in the future. This means that you’ll pay more if your home appreciates in value over time and less if it depreciates.

How Does Unlock Compare With Other Home Equity Products?

If you are looking for other ways to access your home equity, you might consider a home equity loan or a home equity line of credit (HELOC). These are traditional home equity products that allow you to borrow money against your home equity and pay it back over time with interest. However, they have some drawbacks compared to a HEA with Unlock. Here are some of the differences between them:

- A home equity loan or a HELOC requires you to have good credit and sufficient income to qualify. a HEA with Unlock does not have these requirements.

- A home equity loan or a HELOC charges you interest and requires you to make monthly payments on the money you borrow. A HEA with Unlock does not charge interest or require monthly payments.

- A home equity loan or a HELOC has a fixed term and amount that you have to pay back regardless of your home’s future value. A HEA with Unlock has a flexible term and amount that depends on your home’s future value.

- A home equity loan or a HELOC doesn’t share the risk of your home losing value over time. That means you’ll have to pay back the loan amount plus interest regardless. A HEA with Unlock shares both the risk and reward of your home’s future value with you, so if your home loses value, you’ll pay less money back. This can significantly alleviate the financial stress a falling real estate market can cause on homeowners.

Unlock Customer Reviews

One of the best ways to learn more about Unlock is to read what their customers have to say about their experience with them. Here are some of the customer reviews from Trustpilot that show how Unlock has helped homeowners access their home equity without taking on debt:

- “Unlock is the best of the best they are friendly and do what they say they will do I give them 10 stars! My loan manager Shawn was great I recommend to anyone!” – James Morgan

- “The time and fluidity of this process wasn’t as easy as I read and saw from other reviews; however, the service provided made this experience so much more than just a “thanks for your help good job”!! I experienced multiple barriers throughout this process, and each person I dealt with was not only professional and prompt, but took the time to address each issue with me in detail, explain how or why we were seeing it, and provided guidance if I needed to do something or offered to take charge and obtain whatever was necessary to continue! Due to this it took a little longer than I anticipated, but still closed and funded quicker than any of the competition! The people involved made this process worth while, I am just as happy if not happier with my HEL experience as if there were zero issues. I would highly recommend to anyone looking. Special thanks and gratitude to Catrina, Veronica, John Z, and Marcia with Etitle!” – Matt G

- “I want to thank the entire team for doing a great job. Specifically Shelly Sandoval and Laura Costantino, they both explained and lead us through the process seamlessly. Thanks again to the Unlock team, and I will be sending referrals your way.” – Johnnie

- “I was pleasantly surprised by the experience I had from beginning to end. Steve was great, he was very professional, courteous and explained everything. He always returned my calls and texts timely. I felt really confident that I was working with a company that I could trust.” – Jennifer Howai

The Bottom Line

Unlock is a real estate investment company that offers home equity agreements or HEAs to homeowners who want to access their home equity without taking on debt. With a HEA with Unlock, you agree to share a percentage of your home’s future value with Unlock when you sell your home or at the end of the term, which is typically 10 years. You don’t have to pay any interest or monthly payments on the cash you receive from Unlock. You only need to have at least 30% equity in your home and a minimum FICO score of 500 to qualify for a HEA with Unlock.

Unlock is a great option for homeowners who want to access their home equity without adding financial stress or risk. It’s especially suitable for homeowners who have bad credit, low income, or irregular income sources and who need cash for any purpose. It’s the ideal solution for those who want to avoid interest and monthly payments, are willing to share some of their home’s future value with Unlock and plan to sell their home or buy out their agreement within 10 years.

Unlock isn’t an option for homeowners with a recent mortgage. It’s also not a good fit for homeowners who want to keep all of their home’s equity and appreciation potential and don’t want to pay an origination fee and other costs upfront. If you don’t plan to sell your home or pay back your mortgage within the next 10 years, then Unlock may not be for you. If you have good credit and prefer to pay interest and monthly payments on a fixed term and amount, a more traditional home equity product like a HELOC may be a better choice.

Unlock FAQs

How much does Unlock cost?

Unlock does not charge any interest or monthly payments on the cash you receive from them. However, you will pay a 4.9% origination fee and other third-party costs upfront, which will reduce the amount of cash you receive from them. You will also pay back a percentage of your home’s future value to Unlock when you sell your home or at the end of the term, which is agreed upon upfront.

Is Unlock worth it?

Yes, Unlock is worth it if you want to access your home equity without taking on debt or paying interest or monthly payments. Unlock can help you achieve your financial goals, such as paying off debt, funding a home improvement project, starting a business, investing in education, or boosting your savings. Unlock can also help you avoid financial stress or risk, as you do not have to worry about qualifying for a loan, making monthly payments, or paying back a fixed amount regardless of your home’s future value.

Is Unlock safe?

Yes, Unlock is safe and legitimate. Unlock is a licensed real estate investment company that complies with all state and federal laws and regulations. It also uses encryption and security measures to protect your personal and financial information. Unlock has an A+ rating from the Better Business Bureau and a 4.5-star rating from Trustpilot based on 435 customer reviews as of writing this post.

How does Unlock make money?

Unlock makes money by sharing a percentage of your home’s future value with you when you sell your home or at the end of the term. For example, if you receive 10% of your home’s value today from Unlock, you might pay back 18.5% of your home’s value in the future. The difference between these percentages is how Unlock makes money. That money will increase if your home appreciates, but it will decrease if it depreciates over time.